I was right about GM story not being a big deal

yesterday I tried to submit this article to seeking alpha but not surprisingly it was rejected. When It was written the dow was down 300 points. Now it’s up 150 points at only 8:30AM pacific since then because I’m almost always right about economics and stocks. When I say GM story not a big deal, I’m right.

Here is the article:

Title: The Failure of GM Will Have Little Impact on the EconomyAuthor: Cetin Hakimoglu

Positions: Google, Mastercard, Potash Corporation

I turned on the TV at around 3:00 AM on Monday morning to see that futures had tanked. Apparently the General Motors CEO Rick Wagner was forced to step down by the Obama administration, and in addition new details regarding possible bankruptcy in the near term time frame were revealed. However, I knew immediately that this sell off was indeed unjustified because the significance of GM’s contribution to the United State’s economy is being blown out of proportion.

With the Dow down almost 300 points in midday trading, I ask why are people panicking? Why is this this General Motors story so important? Why should a company with a market cap of only a couple billion dollars drag the entire multi trillion dollar stock market down three percent? None of this makes any sense. The US economy is like a painting, and GM represents just a brushstroke.

GM has about 250,000 US employees. In the worst case scenario, If GM were to close completely these people would be unemployed, which seems bad on the surface, until you put the number into perspective. The United States workforce is over 150 million strong, so if all these workers were fired, the total unemployment rate of the United States would rise just a fraction of a percent. GM’s market cap is only a couple billion, so it’s contribution to the DOW and S&P 500 is negligible. Many of these workers will look for work, so it’s not like the unemployment is permanent.

Yes, I know a lot readers from the leftish side of the political spectrum, as well as fringe Ron Paul supporters from the paleoconservative movement like to reminisce of a bygone era when a highschool graduate could make a good living with a unionized manufacutring job, but those days are long gone. The era of American factory jobs and unions are coming to an end.

In the past thirty years a seismic transition from an economy based on the production of manufactured goods to one of production of intellectual (Internet services, software, movies ) and service (fast food, health care, landscaper) goods has occurred. The growth and strength of the US economy isn’t in unionized, entitlement based jobs, but in the meritocracy embodied by the Internet, service, and finance sectors where lifetime employment and pensions subsidized at the expense of the company aren’t a guarantee. But in exchange, companies like Google, Apple, Amazon.com, Visa, Twitter, Wallmart, Myspace, Facebook are created. These are just some examples of companies that contribute greatly to the US economy, while spurring further innovation, as opposed to companies like GM that hold America back.

In conclusion, I would interpret Monday’s sell off as a prime buying opportunity in what has been an exceptional, three week bull market. People are panicking over what will amount to almost nothing should the worse case scenario occur regarding GM. The failure of GM may seem like a big deal according to the headlines, but in actually it isn’t.

Keep Buying the Dips

Title: Keep buying the dips

Author: Cetin Hakimoglu

Positions: Google, Mastercard, Potash Corporation

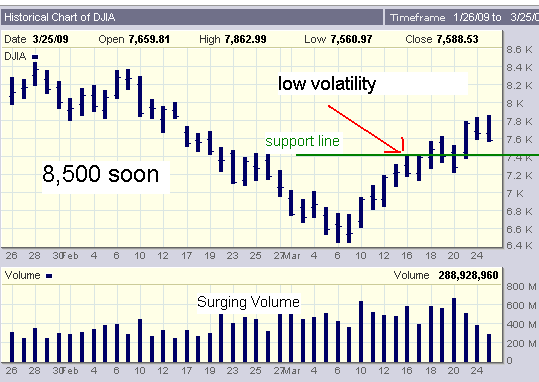

After the phenomenal 6.5 percent rally on March 23 stocks have taken a small breather. While most short sellers are rejoicing in this small victory, the celebration will be short lived as the rally continues. I emphatically believe that we’re in a new bull market that will last for many years, and thus every dips should indeed be bought on the way up.

The trend of low volatility continues. Since this bull market began three weeks ago there have been no major sell offs. The steepest one day sell of has been less than two percent, which is a testament to the unmitigated strength and resiliency of this bull market.

If we compare this bull market to the one that began in 2003 we see many similarities with regards to the cessation of volatility. The chart below shows how the 2003-2007 bull market began. Essentially all the volatility dried up as soon as the bull market began. The pink circle indicates where we are now relative to the last bull market. As you can see, the major breakout has happened and its just a steady, uninterrupted climb higher from here on out

The same pattern can be seen today:

The recent sell off only managed to erase just 90 minutes of the March 23rd rally. It’s nothing more than a minor pullback.

Now is the time to be buying all this dips. We’re in a new bull market, and the best way to make money in such circumstances is to go with the flow rather than resist it. The wall of worry is also intact because the market has yet to sell off on any economic data for the past three weeks. I still recommend google, apple, mastercard, potash corp, mosaic, bidu, and rimm.

What the New Bull Market Will Look Like

itle: What the New Bull Market Looks Like

Author: Cetin Hakimoglu

Positions: Google, Potash Corporation, Mastercard

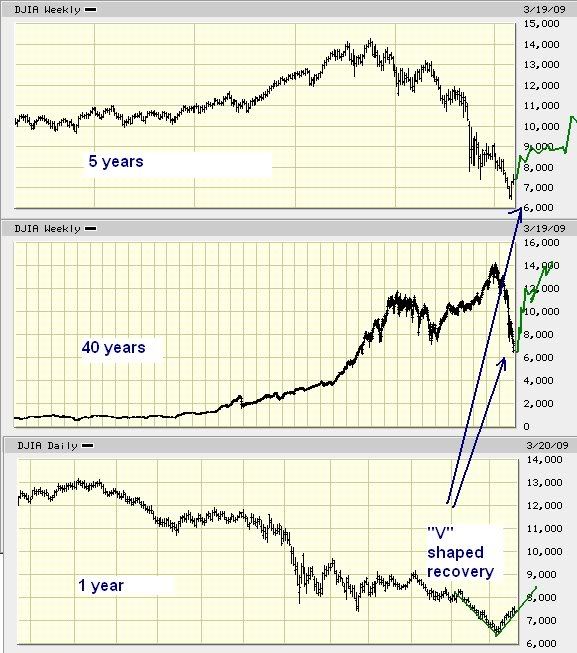

A few week ago I wrote how the recovery in the markets would be ‘V’ shaped. What that means is that the rally in the major indexes would mirror the selloff at the nadir, hence exhibiting symmetry.

On Monday, March 23rd, the rally resumed yet again with unrelenting force on the heels of gains made in the prior two weeks. At this rate, we’ll easily end the week higher for the third time in a row. In my first article on seeking alpha (http://seekingalpha.com/article/123797-the-story-s-still-the-same-but-prices-have-changed), I warned that many short sellers would lose their shirts on the way up as a new bull market begins, and that seems to be the case now.

Regarding the prospects of the market, here is how I picture the rebound of the DJIA to 14,000 playing out:

The chart on the bottom is where we are now. As you you can see, there exists symmetry in each of these time frames at the nadir. Interestingly, these screen shots were taken last Friday before Monday’s huge rally.

Here is another chart showing how the DJIA rallied from 2003 to 3004 when it gained 40%. As you can see, there were few major dips or breakouts; just a steady march higher once the bottom was made in March 2003:

The next chart shows how these steady gains in addition to low low volatility can persist for many years as in the last bull market:

The current bull market, which we’re in now will also play out in this way.

In conclusion, I emphatically believe that the market will indeed recoup all its losses within a few years, and this is because the US economy is still fundamentally strong (link:http://seekingalpha.com/article/124256-a-deep-recession-no-the-most-over-hyped-yes) believe it or not. PE ratios are extremely depressed due to lack of investor confidence, thus if the S&P 500 had a PE ratio of 20 instead of 13 it would be trading at 1,250 now. I’m still recommending buying stocks that benefit from a falling dollar, globalization, and rising commodity prices such as Google, Apple, Research In Motion, Mosaic Corporation, Mastercard, Potash Corporation, Visa, and Bidu.

Debt isn’t bad for the economy

A rebuttal of “Added Debt Won’t Rescue the Great American Ponzi Scheme”

I would like to afford myself the opportunity to rebut Rolfe Winkler, CFA article regarding how the United States is hopelessly mired in a ponzi scheme of debt. American ponzi scheme of debt

There are still many populist misconceptions and myths regarding the deficit and its relation to the sustainability of the US economy, especially in the wake of this supposed financial crisis, and I hope to debunk some of them with my critique. My analysis is italicized.

Original article begins:

Policy-makers not only misunderstand the economic crisis, they continue to underestimate it. Consequently, solutions to date have not only failed to ?fix? anything, they have made the problem worse. The problem isn?t falling asset prices, it?s not rising foreclosures, it?s too much debt.

It is still far too early to write off Geithner’s, Summer’s and Obama’s plans as failures just because the economic outlook may appear cloudy at this present time. Keep in mind that the great depression was exacerbated partially because the government didn’t inject liquidity to stabilize the banking system. FDIC insurance, a United States government corporation, for example, is preventing bank runs from occurring in this current ‘crisis’.

Also, lets assume that in a hypothetical parallel universe nothing is done at all. No bailouts and no stimulus. Would the economy on this parallel earth be any better than on our planet? Would the DJIA be higher today in that parallel earth because the government did nothing? We have no way of proving the answer is ‘no’. But history in the case of the great depression has shown that bailouts and stimulus do work.

With an assist from mark-to-market accounting,* too much debt inflated the asset bubble in the first place. Yves Smith has it exactly right that the only ?solution? to this crisis is price discovery, to allow asset prices to fall to whatever level they need to in order for markets to clear. This is bad news for over-levered balance sheets, but there?s nothing else to be done.

True, asset prices have fallen as evidenced by the decline in housing prices. That’s the free market at work.

And yet American policy-makers appear convinced that more debt can rescue an economy already drowning in it. If we can just keep the leverage party going, all will be well. $787 billion to fund ?stimulus,? another $9 trillion committed to guarantee bad debts, 0% interest rates and quantitative easing to drive more lending, new off balance sheet vehicles to hide from the public the toxic assets they?ve absorbed. All of it to be funded with debt, most of it the responsibility of taxpayers.

The current nation debt to GDP ratio is high, but it’s always been that way as indicated by the graph below:

.

.

It peaked in WW2 and is now rising steadily. With Obama’s stimulus plans it is expected to reach record levels, but this does not imply there will be a subsequent decline in economic activity or the stock market. There is no correlation between high debt and bear markets or economic malaise.

The chart below shows how economic growth historically has been nearly uninterrupted trajectory despite persistent debt:

The reason why this is possible is because the debt helps grow the economy when used to pay for tax cuts, wars, stimulus, and bailouts.

Secondly, tax payers won’ t have to pay because, for one, the Chinese will continue to buy our treasury bonds. Federal income taxes have not increased a penny since George W. Bush’s original tax cuts. I have written more extensively regarding this here http://seekingalpha.com/article/125351-i-think-geithner-and-co-are-doing-a-good-job

If I may offer just one reason this will all fail: rising interest rates. Interest rates need only revert to their historical median in order to hammer asset values, and balance sheets, into oblivion. (click on chart to enlarge)

A simple present value calculation suggests that house prices could fall another 30% if mortgage rates get back to 8%.** Enough to wipe out a 20% down payment made today and still leave the buyer upside down on his mortgage. Given the pile of Treasurys the Obama administration plans to dump on the market, it seems logical to assume interest rates are headed up.

That is a huge ‘what if’…mortgage rates won’t surge because of globalization and the fed’s propensity to print money and the Chinese’s dependency on US treasuries. Keep in mind that the US economy is closer to deflation than inflation according to CPI data, which makes the odds of a sudden surge in mortgage rates extremely unlikely.

In addition, inflation is caused by too much money chasing too few goods. The money being created is being used by the banks to shore up their balance sheets and facilitate landing, which will furthermore help keep a lid on interest rates.

Some might argue that deleveraging is SO violent that a couple years of ?stimulus? and other debt-financed rescue measures are needed to cushion the blow. Unfortunately, any positive impact is likely to be offset by upward pressure on interest rates. Perhaps the Fed can monetize a lot more debt. But that will have its own negative consequences.

Picture it if you will: the economy stabilizes, money flows out of Treasurys, which drives interest rates back to normal. Asset values that had appeared to stabilize fall again. More writedowns ensue, more balance sheets turn up insolvent. The debt deflation conflagration ignites again, burning up what?s left of the economy.

There is no evidence money will flow out of treasuries because China needs the buy our debt to prevent a trade war, civil unrest, and to park their surplus. Interest rates could raise to three percent when the economy does improve, as has happened in prior recession without a snowball effect occurring.

Rising interest rates generally correlates with rising asset values. If money flows out of treasuries inflation will result.

f our experience to date has taught us anything it should be that kicking losses up to bigger balance sheets solves nothing. Losses have to be taken. The balance sheets on which they reside will end up insolvent. Why compound our problems by piling up more debt and concentrating all of it on the public?s balance sheet? Is American arrogance so great that we believe our Treasury and our currency will survive the trillions of $ worth of losses and stimulus we?ve already agreed to fund? To borrow Martin Wolf?s wonderfully evocative phrase, we are a python that has swallowed a hippopotamus.

At the end of the day, flushing more debt through the system is the only lever policy-makers know how to pull. Lower interest rates, quantitative easing, deficit spending, it?s all the same. It?s all borrowing against future income.

Once again, the charts indicate the US economy and stock market has boomed despite persistent debt. Tax cuts and other manifestations of deficit spending are used to grow the economy which subsequently helps pay down the debt. Borrowing against future income is how lending works.

Each time we bump up against recession, we borrow a bit more to keep the economy going. With garden variety recessions, this can work. Everyone wants the good times to continue, so no one demands debts be paid back. Creditors accept more IOUs and economic ?growth? continues apace. If it sounds like Bernie Madoff?s Ponzi scheme, that?s because it is.

That’s fundamental macro economics. Recessions lead to deflation, which is fixed by increasing the money supply. It has nothing to do with ponzi schemes because wealth stemming from businesses, contractors, real estate, ect is being created.

Each time Bernie?s scam got a few too many investor withdrawals, he?d simply plug the hole by raising more investor cash. The guys at Fairfield Greenwich were making so much in fees, they were happy to funnel more his way. But at a certain point, Ponzis get too big. There simply aren?t enough new investors to pay off older ones. In the aggregate, the same is true for Western economies. Their debt loads are now so huge, they are simply unpayable.

Again, the historic debt has remained high, but stable. Although it may reach WW2 percentage levels, this by any stretch of the imagination isn’t catastrophic. The US economy boomed after WW2, while debt was elevated. This is because the debt was used to create wealth, with the benfciearies being defense companies. This wealth eventually tricked down to the american people, leading to a higher post war standard of living, blistering economic growth, and subsequent reduction of the debt.

Naturally, policy-makers sound just like Ponzi-schemers: Just give us a little more cash to get us through this rough patch and everything will be copacetic. Ben Bernkanke at the National Press Club alluded to the famous quote by St. Augustine: ?Oh Lord, give me chastity, but do not give it yet.? President Obama convened his ?fiscal responsibility? summit days after passing the stimulus bill and days before proposing huge increases in health care spending.

Fiscal responsibility tends to be a low priority in recessions because inflating the money supply is how you end recessions. All economic indicators point to deflation. This isn’t a repeat of the early 80’s and 70’s. It would be disastrous fed policy to raise rates or withhold liquidity.

great unwind?

There has been much protest from economists that whatever economic funk we find ourselves in presently, it?s not as severe as the Depression. One data point suggesting otherwise is Household Debt vs. GDP. A favorite example of mine, though, was the chart above featured in the Congressional Oversight Panel?s January report. (Click to enlarge)

The chart downplays our current crisis by comparing the number of failed banks during the Depression with the number today. But the number of bank failures misses the point. The banking system is far more concentrated today. What makes our current banking crisis totally unprecedented is the size of bank failures relative to the overall economy. A better way to compare the two crises is to look at deposits in failed banks relative to GDP. (click to enlarge)

Keep in mind that during the great depression due to the proceeding excess in the stock market banks were created solely to provide funds to speculators to invest on margin. That partially attributed to the excess in failures. Margin requirements in those days were only 10%, but nowadays it’s much higher.

Regarding size concentration of banks, that’s precisely why the government is bailing out the major banks-to prevent a depression like scenario from unfolding. Obviously policy makes are aware that the economic situation will worsen if major banks are allowed to fail.

As you can see, I?ve taken the liberty of adjusting FDIC?s figure for 2008. This chart includes the $2.0 trillion worth of deposits at BofA (BAC), Citi (C), and Wachovia (WB) as of September 30, 2008.***

That’s why these banks are being bailed out.

Last year WaMu was the only ultra-large bank that officially ?failed? according to FDIC. But in the absence of government intervention, it?s likely the entire U.S. banking system would have gone under. Certainly the ?failed? list would now include Citi, BofA and Wachovia.

Adding these three banks to the list still understates the scale of the crisis. Can anyone seriously argue that Chase (JPM) and Wells (WFC) would have survived the year in the absence of taxpayer largess?

We can’t rewrite history. The banks got bailed out, and it does little good to dwell on hypotheticals beyond our control.

What about non-deposit taking financials? AIG (AIG), Fannie (FNM), Freddie (FRE), Goldman Sachs (GS), Morgan Stanley (MS), GE (GE) and?at some point soon?a few of the Federal Home Loan Banks. Then there?s the insurance industry. With leverage worse than the banking system?s and balance sheets chock-full ?o toxic assets, it too owes its survival to publicly-subsidized lending and regulatory ?forbearance.?

Also FDIC?s Deposit Insurance Fund. The $19 billion it has in reserve is but a drop in the bucket compared to the $5 trillion worth of deposits and bank debt it now ?guarantees.? Naturally, the Fund needs replenishing.

Another big ‘what if’..Doomsayers have been forecasting a credit card crunch for the past year, which has shown no signs of actually happening. Obviously if more money were needed in FDIC the treasury department could give it to them with little consequence.

The great Ponzi scheme that is the Western World?s economy has grown so big there?s simply no ?fixing? it. Flushing more debt through the system would be like giving Madoff a few billion to tide him over. Or like adding another floor to the Tower of Babel. To what end? The collapse is already here. The question is: How much do we want it to hurt?

Using the public?s purse to finance ?confidence? in a system that is already kaput may delay the Day of Reckoning, sure, but at the cost of multiplying our losses. Perhaps fantastically.

I, and many other reasonable folks can attest that there will be no such Day of Reckoning. The ponzi analogy is wrong because ponzi schemes don’t actually create welath, while an economy does. A ponzi scheme is insolvent because there is no way way to pay interest or ‘returns’ to the creditors. The United States can theoretically amass an arbitrary amount of debt as long as it can pay the interest though wealth creation, has it has demonstrated historically .

Bottom line?.We can bankrupt ourselves propping up a system that is collapsing anyway, or we can dig ourselves out of debt, if not with higher interest rates then certainly with fiscal austerity. That would be a hard sell to the American people, I know. But deep down, Summers and Geithner know it is the right thing to do. It is, after all, the prescription they wrote for emerging markets facing financial crises.

It?s long past time we took our own medicine. If we don?t take it voluntarily, the bond market will stuff it down our throat anyway.

Disagree. Geithner and Summers are doing a good job. It would be reckless of them to sit idely when macroeconomic conditions and indicators demand more stimulus, liquidity, and bailouts.

In conclusion, I hope through this critique I provided an alternative viewpoint regarding the predominant hawkish sentiment regarding debt. The most important points to take away is that rising or persistent deficits doesn’t necessarily correlate with economic malaise; the US economy has and will continue to thrive with high debt loads. Also, bailing out the ‘too big to fail’ banks providing stimulus though tax cuts will improve investor and consumer sentiment. Third, deflation, not inflation is a concern, which necessitates deficit spending.